Hey everyone, BucksPouds here! I’ve been planning this day in my head for over 2 years now and I am really happy to say that today is the day! My blog is finally live! Yeeeey!

I will be documenting the journey to my first £1m / $1m. Hopefully, £1m will only be the first milestone.

Few words on my background.

I turned 36 just about a month ago, married, and have3 kids. I currently work as a Finance Manager for one of the large US tech companies. Live in South East of England but was born and grew up in one of the ex-Soviet Union countries and moved to the UK in March 2014. I will talk more about my background in one of the future posts.

And now let’s move on to my assets

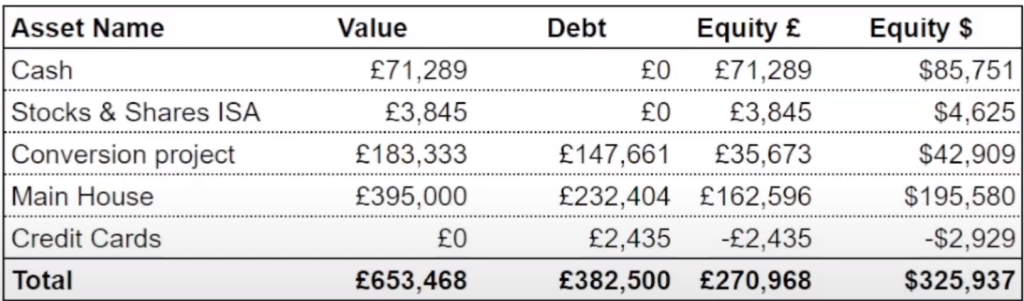

Asset 1. Cash. Very straightforward asset. I have £70,000 in savings ready to be invested. I already have plans on how to invest this money. Probably worth talking about the plan in a separate post (spoiler – property investment). At the moment this is a pure asset and there are no liabilities against it.

Asset 2. Stocks. In February 2021 I opened my first Stocks and Shares ISA account (the UK equivalent of the USA’s Roth IRA). I’ve been adding a little bit every month. By July 2021 I invested exactly £8,000. Everything was going well. I was trading relatively actively and my account balance got to £9,667 at its peak. Almost 21% return in about 6-7 months – not bad for the guy who just opened his first investment account. But then, everything changed in the stock market. I was trading tech stocks and in October 2021 I invested in Paypal and Corsair. PayPal is down 60% since then, I sold Corsair for a massive loss and bought Palantir which is down 38% since I bought it. And as of today, my portfolio is down almost 59% and the current balance is £4,047. I haven’t traded in the last 7 months after I bought Palantir. I think both PayPal and Palantir are oversold now and both should start growing after the overall market will reverse. I am not adding anything to this account anymore as the overall market is still falling. I will just hold what I have at the moment and will start adding more when the trend in the markets will reverse. No liabilities for this asset as well.

Asset 3. Conversion project. This is where things get more interesting. In the middle of lockdown, me and 2 of my friends bought a commercial unit with planning permission to convert it into 3 flats. We all are equal partners and each of us owns 1/3 of the property. We purchased the property for £385,000, but it ended up costing us £405,000 in total if you add stamp duty, auction, legal and other fees. For now, let’s assume that the property value is still £405,000 (even though we’ve already been offered way more for it), but as the profit is still not realized I will keep it simple. It means that my share is worth £135,000 at the moment (£405,000 / 3 partners). We borrowed £275,000 to purchase and develop this property which means that my portion of the debt on this loan is £91,667. Other than direct property finance also I borrowed some money towards the deposit and the current balance of that loan is £55,994. As you can see my liability on this project is already more than my equity. This is because I am including the property development loan. One of the flats is almost ready to go on the market, other 2 will be ready by the end of October. Once I will have the valuations from the real estate agents I will update this asset column to reflect the real value of this property. This is a very exciting project and it definitely deserves a separate video for it. So stay tuned, I am already on this video.

Asset 3. My main residence. Many people may argue that your main residence is not an asset but a liability. But that is definitely not the case with my home. Short explanation – I am planning to subdivide my house into 2 semi-detached houses and maybe try to get planning permission to build an additional house in the garden. If successful this will definitely create additional equity for me, that is why I consider this an asset. I bought my house in November 2017 for £280,000 and spent another £40K on stamp duty, legals and renovation in order to make it a house where my family could live comfortably. In October 2020 I listed my house for sale, the local estate agent valued it at £375,000. I was happy with the valuation as it meant that if it really sold for £375K I would get tax-free capital gains of £55K in just over 3 years (if sold quickly). At the end of February 2021, I got an offer of £350K which I immediately rejected, then they increased the offer to £355K, which I rejected again. The next day the same buyer came with an offer of £360K which I was going to reject again. I had no plans to sell it for anything below £375K. But my wife found several very attractive options in the area where we wanted to move and she persuaded me to accept £360K so that we could move quickly and the kids could start a new school year at a new school. Bear in mind that during that time (January, February 2021) the UK was in lockdown, and the government allowed the housing market to remain open, but everyone thought that after the stamp duty deadline (31st of March at that point) the property market would crash. Long story short, what ended up happening is that our buyers couldn’t get a mortgage for 4 months and at that point there was no chance that we could move house before September and the kids couldn’t start the new year at the new school. On top of that housing market went absolutely mental! And after 4 months of waiting we decided to pull out of the deal and not sell the house for the time being. Since then the house prices in our area went up by more than 10%. This means that my house now costs at least £396K which is confirmed by Zoopla’s estimate of £394K. So for this exercise, I am going to say that the value of my main house is now £396K. The outstanding mortgage is £232,205.79. Which means that I have £163,794.21 of equity in it.

Now let’s move on to my other liabilities

I have 2 credit cards that I fully pay off every month. The current total balance on both cards is £1,721. As I said I always pay off my credit card balance before they start charging interest. Will pay off the current balance at the end of this month. I never carry forward debt on a credit card and suggest you do the same.

So what do we have at the end? £615,656 in total assets and £251,192 in liabilities. This means that my net worth as of 27/07/2022 is £270,968. In order to get my net worth to £1m I need to multiply it by 3.7 times.

The £1,000,000 mark may look far for now. But I have a clear vision of how to get there quickly. For example, the completion of the conversion project should add about £100K to my net worth. Then I am planning to get planning permission to split my main house into 2 semi-detached houses. If I will get permission the building works should cost me around £70K (with extension). But then 2 semi-detached houses should be worth around £280K each (£560K total). Future value of £560K – £70K of costs – £396K current value = £96K of additional equity. But let’s talk about the plan on how to get to my 1st £1m in the next post.

Thank you guys for reading this. This is my first post and I was completely transparent. I hope you enjoyed it. Please hit the like button and subscribe to follow my journey. Lots of exciting stuff is planned. See you in the next one.